Share

Share Twitter

Twitter E-mail

E-mail Download

Download Print

PrintAttain recurring returns above the cost of capital

STRATEGIC OBJECTIVES

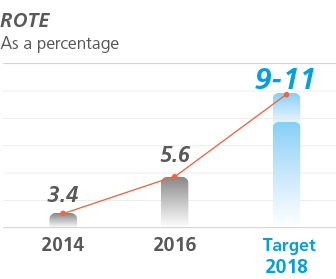

- To achieve a return of between 9% and 11% in ROTE (return on tangible equity) terms in 2018, enhancing the entity’s commercial leadership in the Spanish market.

2016 MILESTONES

Against a backdrop of extreme pressure on profitability, CaixaBank has managed to maintain the strength of its generation of banking revenues, through customer loyalty and diversification of its income base.

Since the launch of the Plan, the entity’s market share for directly deposited salaries and financial advice services (mutual funds, pension plans and savings insurance) have increased significantly, through the development of segmented value propositions for different customer types (caixaBank Negocios, AgroBank, HolaBank and Premier Banking), and a strategic commitment to fostering financial planning for customers (CaixaBankFuturo). The gradual implementation of the new model of A/Store branches has also contributed to specialist advice taking on greater weight in customer relations.

In terms of diversification, in 2016 the entity continued fostering lending for consumption and companies, priority segments for boosting growth in net interest income. Businesses with lower exposure to low interest rates (such as insurance, payment media and asset management) continue to make very strong contributions to Group results.

Efforts continued to contain the cost base, one of the priorities for coming years. In this regard, 2016 saw the launch of a transversal project to optimise organisational structures and processes. The significant reduction in loan-loss provisions resulting from the improvement in credit quality is also contributing to a gradual improvement in profitability.

Overall, the unfavourable backdrop, particularly low interest rates and the weakness of lending volumes, hampered achievement of the initial strategic objectives for profitability. This resulted in a revision of the Plan, adjusting the objectives downwards.

PRIORITIES FOR 2017-2018

- To increase the number of customers and customer loyalty through value propositions based on segmentation and financial advice.

- To boost lending for consumption and companies.

- To contain recurring operating expenses at 2014* levels in 2018.

- To create value in the BPI operation.

Key monitoring metrics

* Includes the pro-forma impact of Barclays Bank, SAU.

FINANCIAL REPORTING AND RESULTS

2016 saw an improvement in efficiency and profitability, based on commercial strength, cost containment and lower cost of risk.

RESULTS

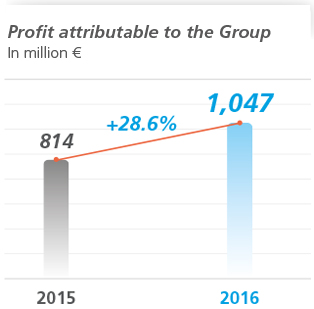

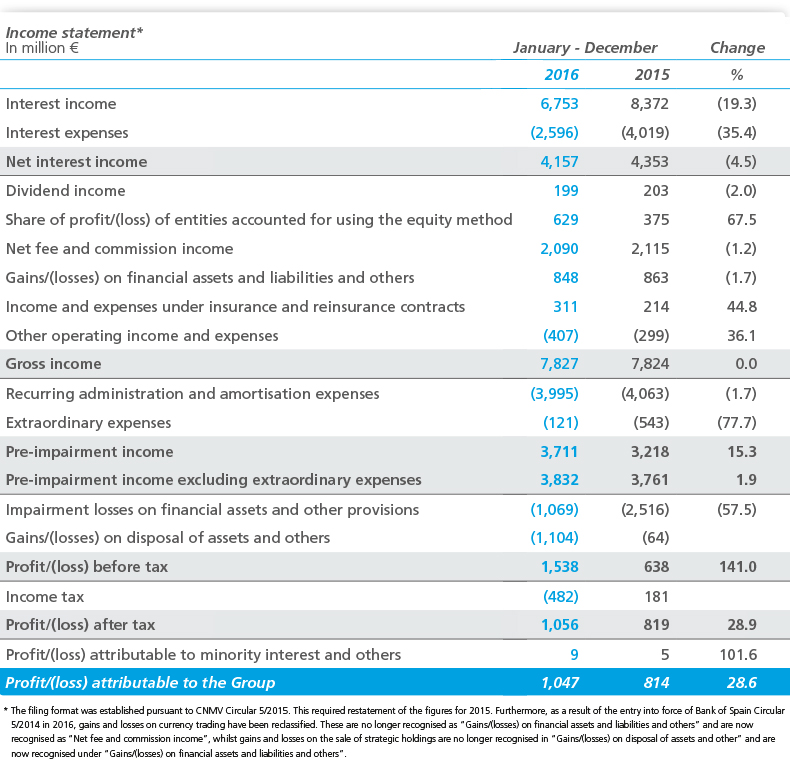

Profit attributable to the Group in 2016 totalled €1,047 million (+28.6% vs. 2015), boosted by the capacity to generate revenues at a time of very low interest rates, rationalisation of costs and lower loan-loss and one-off provisions.

Sustained revenue generation capacity

- Net interest income stood at €4,157 million (–4.5% vs. 2015). This was impacted in particular by lower finance costs for retail savings and institutional finance. It was also due to the contraction of revenues following the reduction in returns on the loan portfolio, as a result of lower market rates and smaller volumes in the fixed income portfolio.

- Revenues from the investee portfolio performed strongly, contributing €828 million (+43.1% vs. 2015).

- Fee and commission income made a strong contribution of €2,090 million (–1.2% vs. 2015) against a backdrop of market volatility at the start of the year, which impacted year-on-year performance.

- The net gain/(loss) on financial assets and liabilities and others amounted to €848 million. These mainly include the materialisation of gains on fixed income assets classified as available-for-sale financial assets.

- There was sustained growth in revenues under insurance contracts, to €311 million (+44.8% vs. 2015) following increased commercial efforts for life-risk insurance.

- Gross income stood at €7,827 million, unchanged on 2015.

million €

income

million €

commissionsmillion €

Efficiency management as a key strategic approach

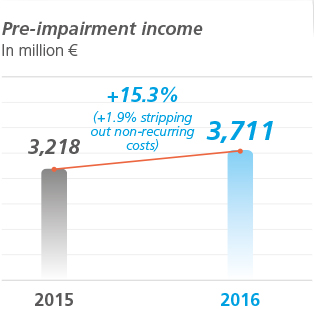

- Recurring costs fell by 1.7% following the capture of synergies and cost reductions.

- 2016 also saw €121 million in non-recurring costs associated with the collective labour agreement signed in the third quarter to optimise the workforce. A total of €543 million associated with the integration of Barclays Bank, SAU and the labour agreement was recognised in 2015.

- Pre-impairment income increased by 15.3% to €3,711 million (+1.9%, excluding non-recurring costs).

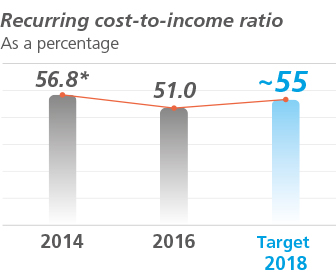

- The recurring cost-to-income ratio improved to 51.0% (–0.9 percentage points).

––0.9 percentage points

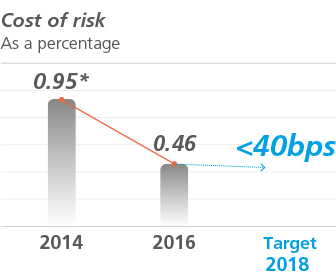

1. Cost of risk of 0.15%, including release of the aforementioned provisions.

Improved credit quality and other impacts

- Reduction of impairment losses on financial and other assets (–57.5% vs. 2015), reflecting the improvement in asset quality indicators and the release of provisions recognised following the development of internal models for credit risk, in line with Circular 4/2016.

- “Gains/(losses) on disposal of assets and others” includes, mainly, proceeds from the sale of assets and write-downs related to the real estate portfolio. Real estate provisions were increased in 2016, following the application of internal models. In 2015, this included the results of non-recurring operations, mainly the negative goodwill generated from the integration of Barclays Bank, SAU, amounting to €602 million.

Floor clauses

- In 2016, the “Other charges to provisions” heading included a provision of €110 million following re-estimation of the present value of disbursements expected to arise from floor clauses. Considering the provisions made in 2015, CaixaBank has provisioned €625 million for liabilities that might arise from these clauses.

- CaixaBank proactively ceased applying floor clauses across practically all of its consumer mortgage portfolio in 2015. Most of these contracts stemmed from entities integrated into CaixaBank over recent years.

- The entity shall apply the measures set out in Royal Decree Act 1/2017, of 20 January, regarding urgent measures to protect consumers affected by floor clauses and shall analyse each claim on a case by case basis.

ACTIVITY

Commercial strength with impressive market shares in the main retail products and services

- Total assets amounted to €347,927 million (+1.1% vs. 2015).

Customer funds

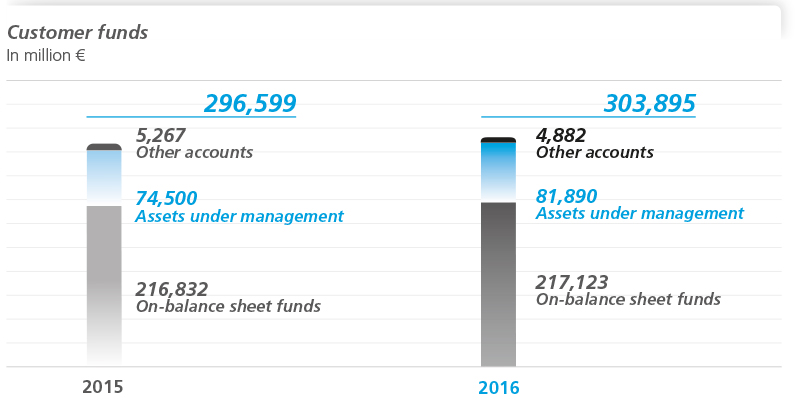

- Customer funds amounted to €303,895 million, an increase or 2.5% on 2015, following intensive commercial efforts.

- The performance of on-balance sheet funds (+0.1% vs. 2015) was fostered by the management of margins on operations; channelling - by savings customers - towards off-balance products; and increased liabilities under insurance contracts (+17.1% vs. 2015), as a result of the success of the CaixaBankFuturo marketing programme.

- Assets under management (mutual funds and pension plans) amounted to €81,889 million (+9.9% vs. 2015), based on the success of the campaigns carried out, the wide range of products offered and the performance of the markets. Net fund subscriptions in 2016 amounted to €4,245 million, 31% of the sector total.

- CaixaBank is the leader for assets under management and the number of mutual fund participants and pension plan assets under management.

(+13% vs. 2015)

Conservative risk coverage policies

The coverage ratio stood at 47%, with provisions of €6,880 million.

Loans and advances to customers

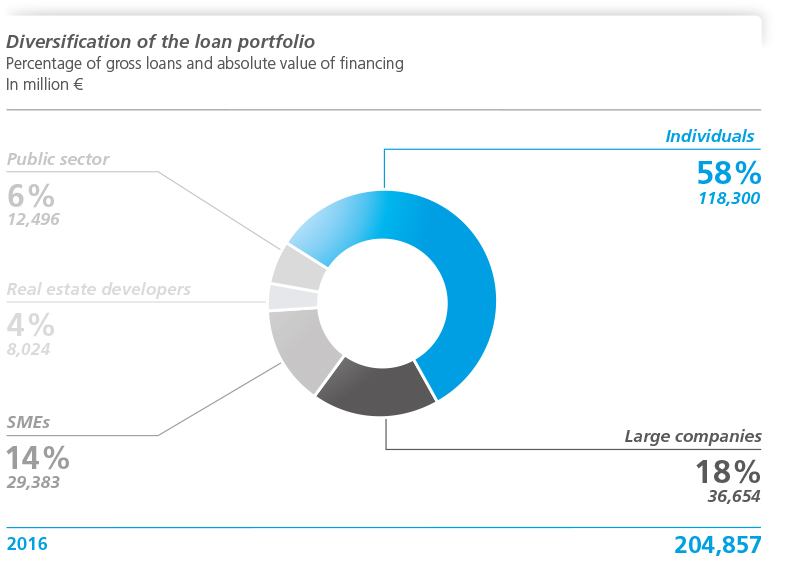

- Gross customer loans and advances stood at €204,857 million. This was impacted (–0.8% in 2016) by household deleveraging, lower exposure in the real estate sector and increased funding of companies, following the success of commercial strategies that enable us to identify profitable business opportunities and respond to the funding needs of customers in these segments.

- There was a 41% increase in the production of new consumer lending following our marketing activities in the year.

- Diversification is one of the key strengths of CaixaBank’s portfolio, 72% of which is dedicated to retail financing (individuals and SMEs).

Excellent liquidity levels

- High-quality liquid assets stood at €50,408 million at 31 December 2016.

- The Loan to Deposits ratio stood at 110.9%, reflecting solid retail financing.

double the minimum 80% requirement from 2017

Note: information to 9 February 2017.