Share

Share Twitter

Twitter E-mail

E-mail Download

Download Print

PrintActive capital management

STRATEGIC OBJECTIVES

- To manage capital actively, anticipating new regulatory requirements.

- To maintain a policy of high and stable dividends (cash pay-out of around 50% of profits).

- To reduce non-performing assets (non-performing loans and foreclosed assets).

2016 MILESTONES

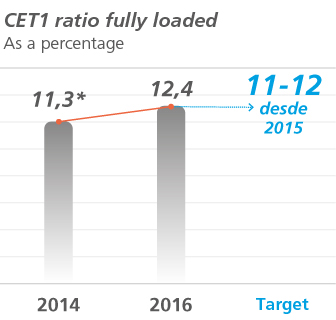

CaixaBank maintained its high levels of solvency. Its fully loaded Common Equity Tier 1 (CET1) ratio stood at 12.4% at 31 December 2016, well in excess of minimum prudential requirements. This robust financial position was once again confirmed in the stress testing carried out by the European Banking Authority and the European Central Bank (ECB) in 2016.

Active management of its holdings has enabled it to comply ahead of schedule with its strategic objective of reducing the capital consumed by its investees to below 10% (standing at under 7% at year-end 2016), through the sale of holdings in Grupo Financiero Inbursa and The Bank of East Asia to CriteriaCaixa.

CaixaBank has continued to pursue its strategic objective of disposing of non-performing assets. The balance of non-performing loans has fallen by 47% since the peaks of June 20131, with a non-performing loan ratio of 6.9% at year-end 2016.

Intensive commercial efforts (real estate sales and leasing) enabled CaixaBank to start reducing its available-for-sale foreclosed assets in 2016, with a reduction of €1,000 million in the year. The margins achieved on the sale of these assets continue to improve, underpinned by improvements in the real-estate market. The disposal of non-performing assets, particularly foreclosed real estate assets, will continue to be a focal point for strategic action over coming years.

1. Includes the pro-forma impact of Barclays Bank, SAU.

PRIORITIES FOR 2017-2018

- To anticipate and adapt to new regulatory requirements.

- To reduce non-performing loans and increase sales of foreclosed assets.

- To foster the highest quality in regulatory, risk and management information.

Key monitoring metrics

* Includes the pro-forma impact of Barclays Bank, SAU.

SOLVENCY

One of the Group’s top priorities is to ensure that its capital is fully optimised

- In 2016, the European Banking Authority (EBA) performed stress tests on leading European banks to assess their capacity to withstand adverse macroeconomic conditions. This exercise was applied to the CriteriaCaixa Group at 31 December 2015. CaixaBank performed an internal estimate applying this methodology, which gave it a Common Equity Tier 1 (CET1) ratio of 9.8% in December 2018 in the regulatory view (8.5% fully loaded). The asset swap formalised in the first half of 2016 between CaixaBank and CriteriaCaixa enhanced this regulatory ratio to 10.1% (9.1% fully loaded).

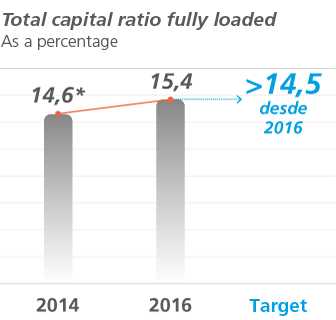

- CaixaBank’s fully loaded CET1 ratio stood at 12.4% on 31 December 2016. Total capital fully loaded stood at 15.4%, and the leverage ratio at 5.4%. Under the progressive application criteria applicable this year, CaixaBank achieved a regulatory CET1 ratio of 13.2%, a total capital ratio of 16.2% and a leverage ratio of 5.7%.

fully loaded

- Risk weighted assets totalled €134,864 million.

- Decisions by the European Central Bank (ECB) and the national supervisor require CaixaBank to have a regulatory CET1 ratio of 9.3125% (including progressive application of the capital-conservation and systemic buffers), rising to 9.5% fully loaded at 31 December 2016. Given the current CET1 ratio, the requirements applicable to CaixaBank would not give rise to any of the automatic limitations set down in solvency regulations regarding distributions of dividends, variable remuneration and interest to holders of additional Tier 1 capital instruments. CaixaBank also complies comfortably with the requirements applicable from 1 January 2017.

ASSET QUALITY

Significant improvement in asset quality

- Non-performing loans (NPLs) fell by €2,346 million in the year.

- This brought the NPL ratio at 31 December 2016 to 6.9% (–1 percentage point vs. 2015). Stripping out the real estate development sector, the NPL ratio stood at 5.9%.

- The main risk segment – lending to individuals for house purchases – features a very diversified portfolio, with strong collateral and a low NPL ratio (4.0%).

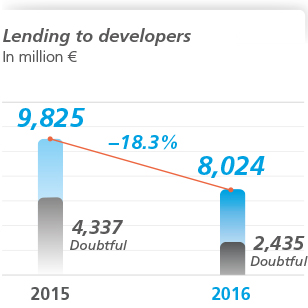

On-going reduction in lending exposure to developers

- 2016 saw a continuation of the downward trend in exposure to the real estate development sector, which fell by 18.3%. The weight of financing for the development sector fell by 84 basis points to 3.9% of the total loan portfolio.

- Finished homes account for 64.7% of the portfolio.

- Coverage for problem assets in this segment stands at 44%.

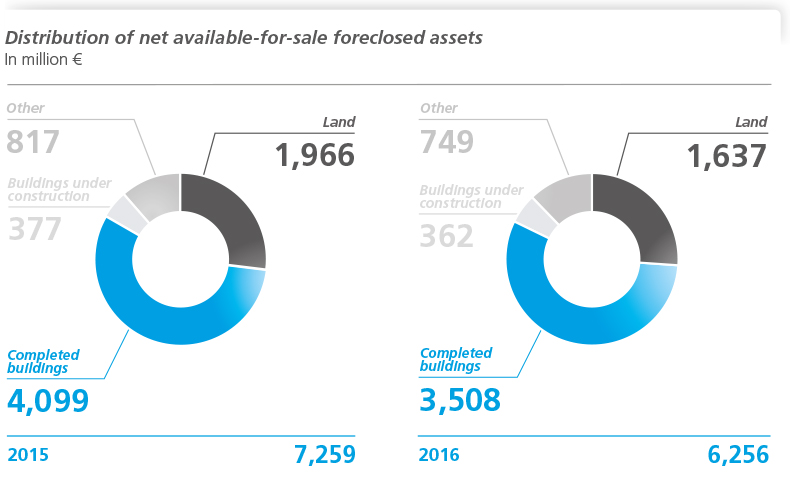

Decrease in the portfolio of foreclosed assets with intensive commercial efforts

- The underlying principle guiding CaixaBank’s management of problem assets is to help borrowers meet their obligations. When the borrower no longer appears to be reasonably able to fulfill these obligations, foreclosure proceedings are initiated.

- Decrease in the carrying amount of available-for-sale foreclosed assets to €6,256 million (–€1,003 million vs. 2015). Coverage increased to 60%.

- In addition, real estate assets held for lease stood at €3,078 million, net of provisions. The occupation rate for this portfolio is 91%.

- Total properties rented or sold amounted to €1,809 million in 2016, with positive returns from sales in the year (5% of the sale price). The composition of the portfolio of available-for-sale foreclosed real estate assets, 56% of which is finished homes, is a unique factor aiding in the sale of these properties on the market.

Properties sold or rented in 2016

million €

million €

million €